The long anticipated draft law 7825 (the “Draft Law”) has been submitted to the Luxembourg Parliament (Chambre des Députés) by the Luxembourg Minister of Finance on 21 May 2021.

If adopted in its current form, the Draft Law will result in substantive amendments to the law of 22 March 2004 on securitisation (the “Securitisation Law”) the purpose of which is to clarify some of the existing rules applicable to securitisation vehicles and to further improve the current legal framework.

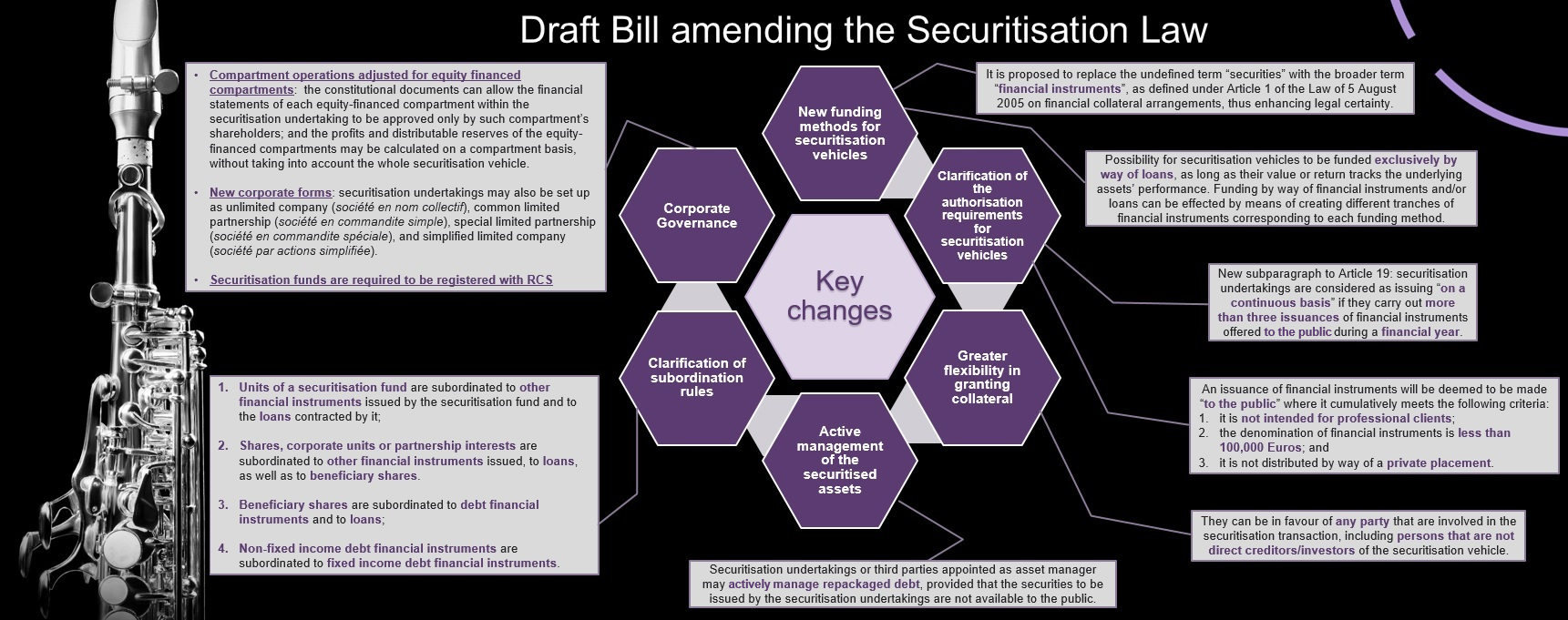

KEY CHANGES IN THE SECURITISATION LAW

-

New funding methods for securitisation vehicles

One of the main proposals under the Draft Law is to amend Article 1 of the Securitisation Law in order to clarify and broaden the existing funding methods available for securitisation vehicles. To this end, it is proposed to replace the currently used undefined term “securities” with a broader term, namely “financial instruments”, as defined under Article 1 of the Law of 5 August 2005 on financial collateral arrangements, thus enhancing legal certainty.

A further novelty is that the Draft Law provides the possibility for the securitisation vehicles to be funded exclusively by way of loans, as long as their value or return tracks the underlying assets’ performance. Funding by way of financial instruments and/or loans can be effected by means of creating different tranches of financial instruments corresponding to each funding method.

-

Clarification of the authorisation requirements for securitisation vehicles

The Securitisation Law requires that a securitisation undertaking issuing securities to the public on a continuous basis be authorised and supervised by the CSSF but does not define the concepts of “issuance to the public” and “on a continuous basis”. With a view to clarifying the CSSF authorisation requirement, the Draft Law introduces a new subparagraph to Article 19 of the Securitisation Law, which states that securitisation undertakings are considered as issuing “on a continuous basis” if they carry out more than three issuances of financial instruments offered to the public during a financial year. The amended Article 19 further clarifies that an issuance of financial instruments will be deemed to be made “to the public” where it cumulatively meets the following criteria:

- it is not intended for professional clients as defined under the law of 5 April 1993 relating to the financial sector;

- the denomination of financial instruments is less than 100,000 Euros (instead of 125,000 Euros as per the current CSSF guidance); and

- it is not distributed by way of a private placement.

The above clarifications reflect the guidance previously provided by the CSSF on this topic under the Frequently Asked Questions.

-

Greater flexibility in granting collateral

Pursuant to Article 61(3) of the Securitisation Law, securitisation undertakings can only create security interests over their assets or provide guarantees in favour of their investors or in order to secure their own obligations assumed for the purposes of securitising the assets. On this point, the Draft Law adopts a more flexible approach by enabling the granting of collateral to secure any obligation relating to a securitisation transaction, which will allow a securitisation vehicle to grant security interests or guarantees in favour of any party that are involved in the securitisation transaction, including persons that are not direct creditors/investors of the securitisation vehicle.

-

Active management of the securitised assets

The Draft Law will introduces a new Article 61-1 to the Securitisation Law, regarding the possibility of a securitisation vehicle to actively manage a securitised debt portfolio. Accordingly, the securitisation undertakings or a third party appointed as asset manager may actively manage repackaged debt, provided that the securities to be issued by the securitisation undertakings are not available to the public.

-

Clarification of subordination rules

The Draft Law also introduces a set of rules on legal subordination, applicable to the financial instruments issued by securitisation undertakings. More specifically, according to these rules:

- Units of a securitisation fund are subordinated to other financial instruments issued by the securitisation fund and to the loans contracted by it;

- Shares, corporate units or partnership interests of a securitisation company are subordinated to other financial instruments issued by such securitisation company, to loans contracted by it, as well as to beneficiary shares issued by it.

- Beneficiary shares issued by a securitisation company are subordinated to debt financial instruments issued by such company and to loans contracted by it;

- Non-fixed income debt financial instruments issued by a securitisation undertaking are subordinated to fixed income debt financial instruments issued by it.

However, securitisation undertakings may derogate from the above rules either contractually or under their constitutional documents.

-

Corporate Governance

The Draft Law envisages certain corporate governance related changes, as below:

- Compartment operations adjusted for equity financed compartments: The Draft Law provides that the constitutional documents of the securitisation vehicles can allow the financial statements of each equity-financed compartment within the securitisation undertaking to be approved only by such compartment’s shareholders; and the profits and distributable reserves of the equity-financed compartments may be calculated on a compartment basis, without taking into account the whole securitisation vehicle.

- New corporate forms available for securitisation vehicles: Under the existing legal regime, securitisation undertakings may only be set up as a public limited company (société anonyme), a corporate partnership limited by shares (société en commandite par actions), a private limited liability company (société à responsabilité limitée) or a co-operative company organised as a public limited company (société cooperative organisée comme une société anonyme). The Draft Law adds to these corporate forms, the unlimited company (société en nom collectif), common limited partnership (société en commandite simple), special limited partnership (société en commandite spéciale), and simplified limited company (société par actions simplifiée).

- Securitisation funds are required to be registered with RCS: Finally, the Draft Law expressly provides the requirement of securitisation funds to be registered with the Luxembourg trade and companies register (Registre de Commerce et des Sociétés) (“RCS”), which currently are not required to be registered with the RCS. The securitisation funds incorporated before the entry into force of the Draft Law will have to comply with this requirement within 6 months of the entry into force of the Draft Law.

Share on

{kind=link}