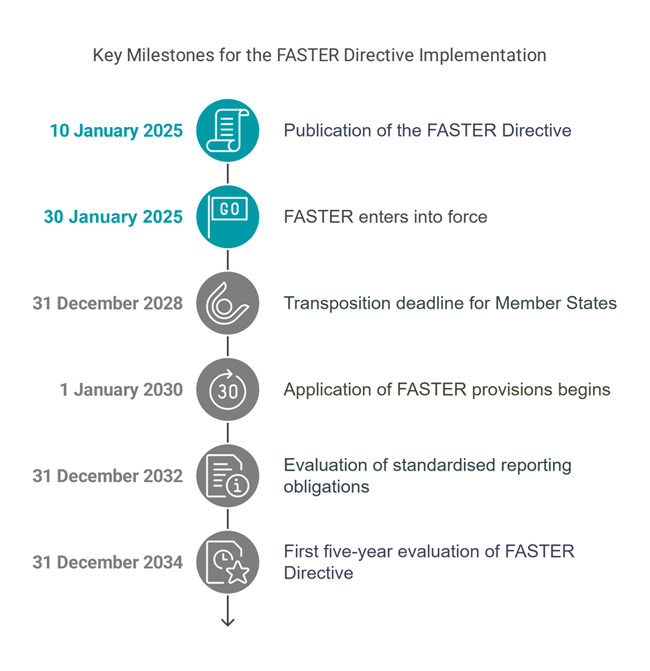

On 10 December 2024, the Council of the European Union (“Council”) formally adopted the Directive for Faster and Safer Relief of Excess Withholding Taxes (“FASTER Directive”). The FASTER Directive was subsequently published in the Official Journal of the European Union on 10 January 2025.

Key Measures Introduced by the FASTER Directive

The FASTER Directive introduces several key measures to streamline and harmonise withholding tax (“WHT”) procedures across EU Member States:

- Fast-track procedures:

- relief-at-source procedure: allows the application of reduced WHT rates or exemptions directly at the time of dividend or interest payment.

- quick refund procedure: ensures refunds for over-withholding are processed within 60 days from the payment date.

- Certified financial intermediaries (“CFIs”):

- CFIs, in collaboration with investors will assist in navigating the fast-track procedures.

- CFIs are required to register in a national register and adhere to standardised reporting obligations to enhance transparency and reduce fraud.

- Digital tax residence certificates (“eTRC”):

- introduction of a harmonized EU digital tax residence certificate, necessary for investors to benefit from the fast-track procedures.

For more information, please refer to our previous newsletter on this topic here.

Next steps - Calendar

The FASTER Directive will enter into force on the 20th day following its publication in the Official Journal, on 30 January 2025.

Member States must transpose the Council Directive into their national legislation by 31 December 2028 and apply the provisions from 1 January 2030.

The Commission shall, by 31 December 2032, evaluate the impact of the mechanisms of standardised reporting obligations applicable to the CFIs and the option not to apply the relief procedure for certain EU Member States.

The Commission shall also, by 31 December 2034 and every five years thereafter, examine and evaluate the functioning of the FASTER Directive, including the potential need to amend specific provisions, and submit a report to the European Parliament and the Council.

Share on