Introduction

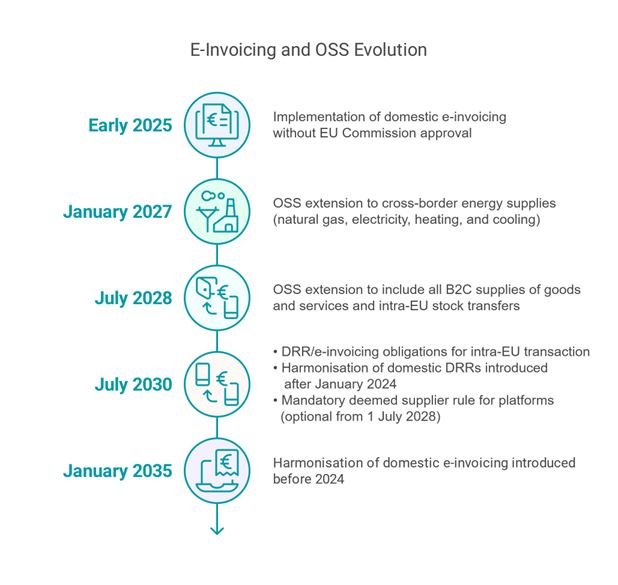

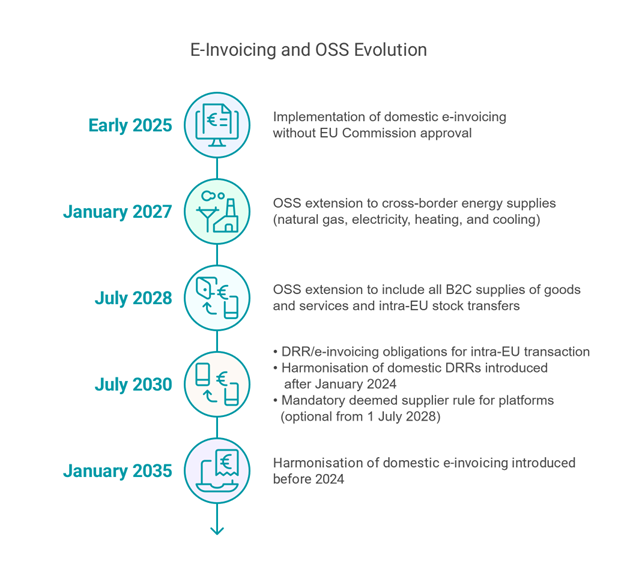

On 5 November 2024, the Council adopted several measures aimed at conforming the value added tax (“VAT”) rules to the digital age. The ViDA package will bring major changes to the VAT system.

The ViDA package is based on three main pillars:

Pillar 1: digital VAT reporting

This first pillar introduces a real-time digital reporting system based on e-invoicing for businesses that operate cross-border within the EU. In practice, an e-invoice will have to be issued for all intra-community B2B supplies of goods and services. In addition, for these transactions, a real-time digital reporting will be introduced. The purpose of this system is to transmit information from taxpayers to the tax authorities in an electronic format, in real time and to ensure that VAT is effectively collected. Member States thereby hope to receive in real-time the information they need to step up the fight against VAT fraud, especially carousel fraud.

Pillar 2: VAT for the platform economy

This second pillar introduces an obligation for platform economy operators providing passenger transport and short-term accommodation to collect and pay VAT to the tax authorities when service providers do not, for example because they are a small business or individual provider. In practice, platforms will be considered as “deemed suppliers”, meaning that they will be considered to receive the relevant service from accommodation or transport supplier and provide this same service to the end-customer. This should ensure a uniform approach across the EU, contribute to a level playing field between online and offline providers and simplify life for SMEs, relieving them from having to understand and comply with VAT rules sometimes throughout several Member States.

Pillar 3: one-stop shop for VAT registration

The aim of this measure is to facilitate VAT registration for businesses operating cross-border within the EU. A single VAT registration system will be established, by leveraging on the existing One-Stop Shop (“OSS”) and Import One-Stop Shop (“IOSS”) systems. This pillar allows companies operating in the European market to register only once and in one language for the entire EU. Fulfilment of VAT obligations is also intended to take place via a single online portal and in one single language. Administrative charges and related costs should thus be reduced by this measure.

Background and next steps

On 8 December 2022, the European Commission issued a legislative proposal concerning VAT in the Digital Age. The Commission’s proposal specifically targets (i) Council directive amending directive 2006/112/EC regarding VAT rules for the digital age, (ii) Council regulation (EU) No 904/2010 as regards the VAT administrative cooperation arrangements needed for the digital age, and (iii) Council implementation regulation amending implementing regulation (EU) No 282/2011 as regards information requirements for certain VAT schemes.

The Commission’s intention is to create a package with a series of measures to modernize the current VAT system to resist against tax fraud and adapt VAT to the digital age.

Originally, the proposal will enter into force gradually between 2024 and 2028. However, the Council has established a new timeline for Member States to adapt the new system between 2031 and 2032.

The text will now go through technical and linguistic checks before being presented to the Council for formal adoption. The texts will then be published in the EU’s Official Journal and enter into force.

For more information, please refer to our previous newsletter on this topic.

Share on

{kind=link}